There’s a sneaky wave in the car industry where auto loans have gradually increased from an average of 36 – 48 months (3-4 years) to the average auto loan in 2019 which was 69 months. That’s 5.75 years.

Ten years ago, car loans averaged 3-4 years, today 5-7 years.

Americans today do not own anything. We have become accustomed to financing our life and buying everything on credit. We pay monthly for our cell phones with top-end phones, costing an excess of $1K. We also finance our TVs, furniture, clothing, and automobiles, to name a few.

If you want it, there’s a payment plan for that.

The trap of the six-year loan

On the surface, the longer your auto loan, the better for you. It benefits you by allowing you to pay the least amount while allowing you to buy a more expensive vehicle that falls in the range that “you can afford.” The “I can afford mentality” is one reason why many Americans are in debt. We want instant gratification, and we want it now, and we don’t want to save to buy it later.

Car Buying Options

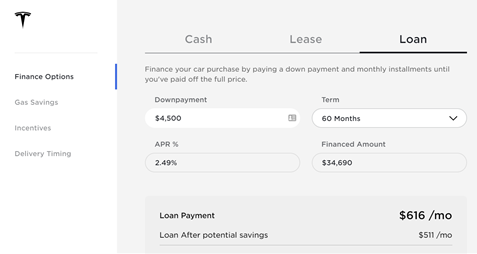

Let’s say you want that brand new Telsa Model 3. https://www.tesla.com/model3

Let’s look at your Financing options.

1. Pay Cash

That is always your best choice. As they say, cash is king. When you pay cash you often can get significant discounts that would not otherwise be passed down to someone who finances. Look at the above price tag, let’s say you only had $30K in cash and you walked into the dealership and said, “this is all I’m willing to pay for the vehicle, take it or leave it.” There’s a good chance they will negotiate with you, as that’s a sale they could make now and they will have the cash in hand. Paying cash simply gives you options.

However, many of us don’t have that kind of money lying around, so we end up leasing or financing. Ideally, if you don’t have the cash to buy your dream car, the goal would be to save and invest until you could afford it. However, this goes back to my earlier point of instant gratification. We want it now. Not later.

2. Leasing: Not necessarily the best option or the worst

The Bad:

- You are financing the vehicle: At the end of the lease, you don’t get to keep the car. That’s the worst outcome.

- Mileage Cap: Looking at the example, the lease term for the Telsa Model 3 caps your mileage at 10K, 12K, or 15K per year. Once you choose a mileage, if you go over that, they will charge you a fee for every mile above what is listed on the contract. This has the potential to add hundreds if not thousands to your lease.

- Always having a car payment: When you lease, you get stuck in the cycle of having a car payment. Instead, you could own, and put that money you would be spending on the monthly lease payments towards your investments.

- You are paying for all the depreciation. After your lease is over, someone can come to buy the vehicle at significantly less since you have already paid for the most expensive part of owning the car.

- If you fall behind on payments or simply can’t afford the payments, your car will be repossessed and negatively affect your credit history.

The Good:

- Low Monthly payments: For most people, if you have good to excellent credit, if you lease a vehicle, you will likely have lower monthly payments. Your out-of-pocket cost to acquire the vehicle is much less, i.e., lower down payment and no sales tax.

- Upgrading to a New Vehicle every few years: I think this is the best reason to lease. Some people like the new car smell and are willing to make payments their whole life. Having the option of a new vehicle every few years is appealing and is the desired lifestyle design for many. It may not make the best financial sense, but if you value it and it fits into your financial goals, who am I to argue?

3. Car Loans/Financing

4 years (48 months) @ $760/month

5 years (60 months) @ $616/month

6 years (72 months) @ $519/month

As you noticed, as the Loan terms get longer from 48 to 72 months, the payments drop significantly. You go from saying, “I can’t pay $760” to thinking “I can do $519 a month”. This mentality has trapped us into paying for things we cannot afford.

You don’t see that, although your payments get smaller, most of the time, your interest rates increase. In general, the longer your financing terms, the higher your interest rates, meaning that you will be paying more interest in the end, thereby spending more on the vehicle. This is significant when the national average for US auto loan interest rates is 5.27% on 60-month loans.

How I got trapped in the six-year car loan

In 2014 after my wife and I found out we were expecting our first child, my wife decided she wanted to upgrade her vehicle. At the time, we were a one-car household, and she was driving a 2009 Nissan Altima. Her father was also looking for a car, and he decided he wanted the Altima. As we were shopping around, we looked for used and new cars, and my wife eventually decided to go with a brand new Jeep Grand Cherokee Overland. This was around the same time I found out I got accepted to medical school. Knowing that she would be the main one working as I pursue medical school, looking back, we did the unthinkable and signed a six-year (72 months) auto loan.

Financially, we were in decent shape; we had excellent credit scores and only had our undergrad student loan debt. We were moving in with her parents as I was getting ready to prepare to start medical school, so financially, we did not have many recurring payments at that time, and we could afford the payments. We were able to secure the auto loan at a 1.99% interest rate.

Looking back, we bought too much car that we simply did not need. It’s funny how our minds work in justifying our mistakes. We anticipated we would need the bigger vehicle as we wanted two-three kids, but we should have waited until we outgrew the Altima before we bought it.

Now that we have two kids, the Jeep does not provide us with any additional spacing that the Altima did not give us. Her father still has the Altima, and we use it at times and it has plenty of space for the car seats and strollers.

After six years, we finally paid off the car loan this year, just a couple of months after my daughter turned six years old. Looking back, this is lunacy.

Why did we go out and spend $42K on a brand new vehicle? We knew better as our original goal was to buy a used car. Yet, we fell into temptations and bought more than we anticipated. Yes, we could afford the payments but, at $632 a month for six years, I think back, if we bought a cheaper vehicle or did not even buy one at all, we could have had more money to invest and pay down debt.

We need to keep in mind what is the point of owning a vehicle. Vehicles are a tool to get us from point A to B. How much you spend on it becomes personal choices. The end goal is still to get from point A to B. The style, comfort, and luxury come at a price. However, that personal choice and cost should not hinder your overall financial plan and success, and you should be cognizant of how much debt you are incurring to get to your final destination.

American marketing is powerful. Subconsciously it makes us want the best, the brand new, and we end up paying for things we don’t need.

Your options: buy a cheaper car that you can afford, buy a used vehicle (certified pre-owned). It’s not sexy (as I think there’s a stigma about buying used items). However, when it comes to buying vehicles, this is the best option for your money. Cars just depreciate too fast, as they say, as soon as you drive it off the dealership lot, it loses 10% of its value. Don’t make the same mistake I made and let someone else pay for that depreciation while you reap the benefits of having a cheaper vehicle with lower payments and still get from point A to B.

{kind=link}